Most people believe saving money on flight tix is all about finding the right deal at the right time.

They compare prices, check different websites, wait for discounts and hope they’re getting the best possible fare.

But here’s what most travelers don’t realize:

The biggest savings don’t come from searching better they come from paying smarter.

Two people can book plane tickets for the exact same flight, on the same day, for the same destination. One pays $600. The other pays $200 or sometimes nothing at all.

Same airline. Same seat. Completely different cost.

The difference isn’t luck, timing, or a secret website.

It’s how they’re using credit cards and travel rewards.

In 2026, credit cards are no longer just a payment method they’re a travel strategy. The right card can help you earn points on everyday spending, unlock massive signup bonuses, access airline partnerships, and convert those rewards into real flight savings.

But this is where most people go wrong.

They either don’t use travel credit cards at all, or they use them without a clear strategy. They collect points slowly, redeem them for low-value rewards like cashback or products, and completely miss the high-value opportunities like discounted or nearly free flights.

So even when they’re earning rewards, they’re not actually saving money.

That’s why many travelers feel like credit card points don’t “work” when in reality, they’re just not being used correctly.

This guide is designed to fix that.

Instead of guessing, you’ll learn which credit cards are actually worth using for cheap flights in the USA, how to maximize points and bonuses, and how to turn your everyday expenses groceries, fuel, bills into travel savings.

By the end, you’ll stop chasing flight deals like everyone else.

You’ll start creating your own discounts every time you book a flight.

✅ Read also : Best Budget Destinations from Chicago (Cheap Flights, Itinerary & Total Trip Cost 2026)

How Credit Cards Help You Get Cheap Flights

Travel credit cards don’t reduce the actual price of a flight but they completely change how you pay for it. Instead of relying only on cash, you’re using a system where your everyday spending turns into points or miles for an aircraft ticket, which can then be redeemed for flights.

Here’s how it works in practice:

- Every time you spend on groceries, fuel, dining, or bills, you earn points or miles

- These points accumulate over time or through signup bonuses

- You redeem those points to reduce the cost of flights or sometimes cover the entire air ticket reservation

- On top of that, many cards offer travel perks like free baggage, priority boarding, or discounts

So instead of paying full price, you’re offsetting the cost using rewards you’ve already earned

Simple Example

- Plane ticket price: $500

- Points used: Equivalent of $350

- Out-of-pocket cost: $150

You save $150 instantly without changing the flight or airline

And in some cases, especially with strong signup bonuses, you can cover the full cost of the ticket.

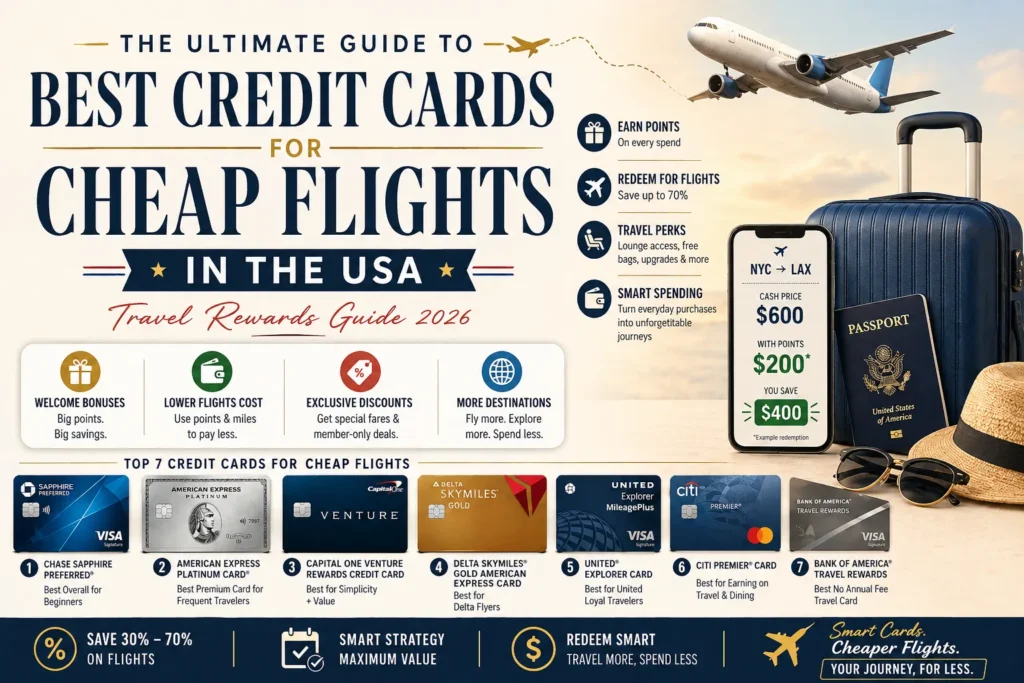

That’s how frequent travelers consistently reduce their flight costs by 30%–70%

Types of Travel Credit Cards

Not all credit cards work the same way. Choosing the right type of card determines how much you can actually save.

1. Airline Credit Cards

These cards are directly linked to a specific airline’s loyalty program.

Examples include:

- Delta Air Lines credit cards

- United Airlines booking credit cards

How they work:

- You earn miles within that airline’s ecosystem

- Rewards are best used for that airline’s flights

Best for: Travelers who consistently fly with one airline

Pros:

- Free checked bags (saves $30–$60 per trip)

- Priority boarding

- Easier redemption within one system

Cons:

- Limited flexibility (you’re tied to one airline)

- Lower value if you don’t fly that airline often

Great if you’re loyal to one airline but restrictive otherwise

2. Flexible Travel Cards

These are the most powerful cards for reducing flight costs because they’re not tied to a single airline.

Examples include:

- Chase Sapphire cards

- American Express travel cards

How they work:

- You earn points in a central rewards system

- You can transfer those points to multiple airlines or book directly

Best for: Travelers who want flexibility and maximum value, including Southwest Airlines ticket reservation

Pros:

- Access to multiple airline partners

- Ability to compare and choose the best redemption

- Higher potential value per point

Cons:

- Requires strategy to maximize benefits

- Slightly more complex to use

This is where serious savings happen if used correctly

3. Cashback Cards

These cards don’t use points or miles they give you cashback on spending.

How they work:

- You earn a percentage of your spending back as cash

- You can use that cash to offset travel costs

Best for: Beginners who want simplicity

Pros:

- Easy to understand and use

- No complex redemption rules

Cons:

- Lower overall value compared to travel rewards

- No travel-specific perks

Good for simplicity but not ideal for maximizing flight savings

✅ Read also : How Far in Advance Should You Book Flights? (2026 Data Guide)

Best Credit Cards for Cheap Flights

Choosing the right credit card is not just about rewards it’s about how efficiently you can convert those rewards into real flight savings. The cards below are among the most effective options for US travelers, including Hawaiian Airlines reservations, depending on your travel style and goals.

1. Chase Sapphire Preferred Best Overall

This is one of the most recommended travel cards, especially for beginners who want strong value without complexity.

Why it stands out:

- High signup bonus (often enough for 1–2 domestic or one international flight)

- Points can be transferred to multiple airline partners

- Strong redemption value through travel portals or transfers

Best for: Travelers who want flexibility and maximum value across different airlines

Key advantage: You’re not locked into one airline, so you can always choose the cheapest or best route

2. American Express Platinum Card Best Premium Travel Card

This card is designed for frequent travelers who want both savings and a premium travel experience.

Why it’s powerful:

- High reward rates on travel bookings

- Access to airport lounges worldwide

- Annual travel credits (for flights, hotels, etc.)

Best for: Frequent flyers who travel multiple times a year

Key advantage: Combines savings with comfort ideal if you value both

3. Capital One Venture Rewards Credit Card Best for Simplicity

If you want a straightforward system without complicated rules, this card is one of the easiest to use.

Why it works:

- Simple earning structure (flat rewards on all spending)

- Easy redemption for travel purchases

- Ability to transfer points to airline partners

Best for: Users who want a balance of simplicity and value

Key advantage: No need to track categories earn consistently on everything

4. Delta SkyMiles Gold American Express Card Best for Delta Flyers

This card is ideal if you frequently fly with Delta.

Why it’s useful:

- Free checked bags (saves $60+ per trip)

- Priority boarding

- Earn miles directly in Delta’s ecosystem

Best for: Travelers loyal to Delta

Key advantage: Saves money on every trip through built-in perks

5. United Explorer Card Best for United Travelers

A strong option for those who regularly fly with United Airlines.

Why it’s effective:

- Earn MileagePlus points

- Free checked bags and priority perks

- Access to United travel benefits

Best for: Frequent United flyers

Key advantage: Maximizes value if you stick to one airline

👉 Not sure which card matches your travel pattern? Compare options here: Click here.

How to Use Credit Cards to Actually Save Money

Most people earn points but don’t extract real value from them. The difference comes from how you use them.

1. Focus on Signup Bonuses First

Signup bonuses are the fastest way to accumulate points.

- Many cards offer bonuses worth $500–$1000 in travel value

- Often enough for 1–2 free flights

This is where most of your savings come from not regular spending

2. Use Points for Flights

One of the biggest mistakes is redeeming points for low-value items like gadgets or vouchers.

- Product redemption = low value per point

- Flight redemption = highest value

Always prioritize flights for maximum return

3. Transfer Points Strategically

Flexible cards allow you to transfer points to airline partners.

- This can unlock cheaper award tickets

- Sometimes gives better value than direct booking

Smart transfers = higher savings per point

4. Combine Points with Low Fare Timing

Don’t just use points anytime, use them strategically.

- Book during off-season or low fare periods

- Combine cheap flights + points

This multiplies your savings

Common Mistakes to Avoid

Even with the right card, poor usage can reduce your savings.

- Redeeming points for low-value rewards

- Ignoring annual fees vs actual benefits

- Not tracking point expiry or redemption value

- Staying loyal to one airline when cheaper options exist

Wrong strategy = lost savings opportunity

Real Example

- Flight price: $600

- Points used: $400 value

- Final cost paid: $200

You save $400 without changing the flight

Key Insight

Credit cards don’t just give rewards they change how you pay for travel

The right card + correct strategy can reduce flight costs by 30%–70%

You’re not just earning points you’re converting everyday spending into travel savings

FAQs

1. Are travel credit cards really worth it for cheap flights?

Yes if used correctly, travel credit cards can significantly reduce your flight costs. The real value comes from signup bonuses, reward points, and travel perks. Many cards offer bonuses that alone can cover 1–2 flights. However, the benefit depends on how you earn and redeem points. Used strategically, they can cut travel costs by 30%–70%

2. Which type of credit card is best for beginners?

For most beginners, flexible travel cards like Chase Sapphire Preferred are ideal. They offer a balance of simplicity and strong rewards, along with the flexibility to book flights across multiple airlines. Start with flexibility before moving into airline-specific cards

3. How do credit card points actually reduce flight costs?

Points act like a currency. You earn them through spending and redeem them to pay for flights. Instead of paying full cash, you offset part (or all) of the ticket using points.

For example:

- Flight cost: $500

- Points used: $350 value

You only pay $150

You’re not getting discounts you’re replacing cash with rewards

4. Can I really get free flights using credit cards?

Yes, especially through signup bonuses. Many cards offer enough points after initial spending to cover a full flight. With consistent use and smart redemption, multiple free or heavily discounted flights are possible each year. Free flights are achievable but require planning and discipline

5. Do travel credit cards have hidden costs or risks?

The main cost is the annual fee, which can range from $95 to $600+. However, if you use the benefits properly (free bags, credits, rewards), the value often outweighs the cost. The biggest risk is overspending just to earn points. The card only works if your spending stays controlled

6. Should I choose airline-specific cards or flexible travel cards?

It depends on your travel behavior:

- Choose airline cards (like Delta Air Lines or United Airlines) if you fly with one airline regularly

- Choose flexible cards if you want the best deals across multiple airlines

Flexibility usually leads to better savings unless you’re loyal to one airline

7. What is the biggest mistake people make with travel credit cards?

The most common mistake is redeeming points for low-value rewards like products, vouchers, or cashback instead of flights. Other mistakes include ignoring transfer options, not tracking points, and not maximizing signup bonuses. Earning points is easy maximizing their value is where most people fail

CONCLUSION

If you’re paying full price for flights in 2026, you’re overpaying. Because the smartest travelers aren’t just searching for deals they’re creating them.

👉 Through credit cards, rewards, and strategy

👉 Not sure how to maximize your credit card for flight savings? Get expert help to find the best deals tailored to your rewards. 📞 +1 (844) 551-9200